(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

(Any views expressed here are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

Want More? Follow the Author on Instagram, LinkedIn and X

Access the Korean language version here: Naver

Subscribe to see the latest Events: Calendar

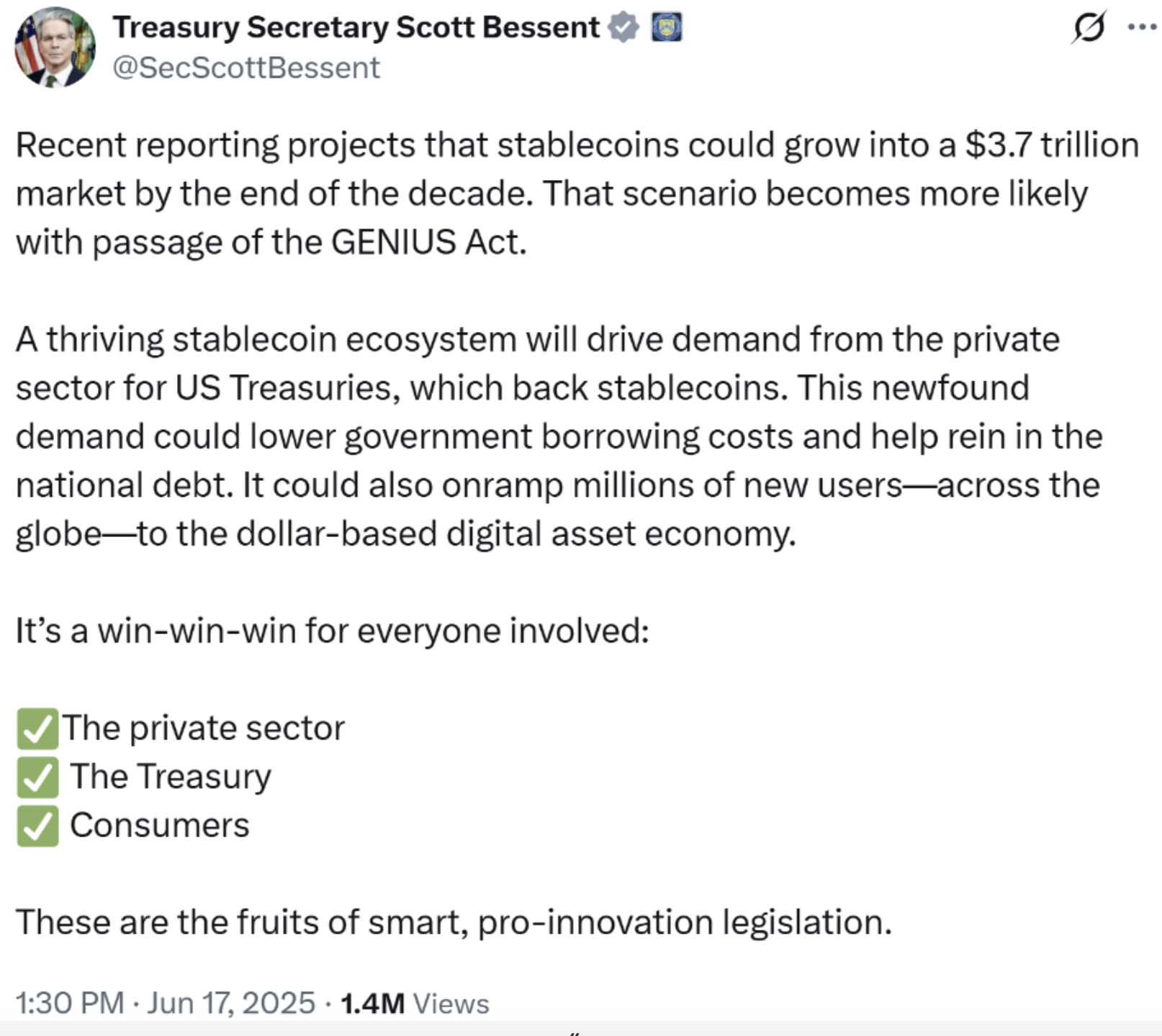

Equity investors be Yellen, “Stablecoin, stablecoin, stablecoin; Circle, Circle, Circle.”

Why are they so bullish? Because The Big Bessent Cock (BBC) said:

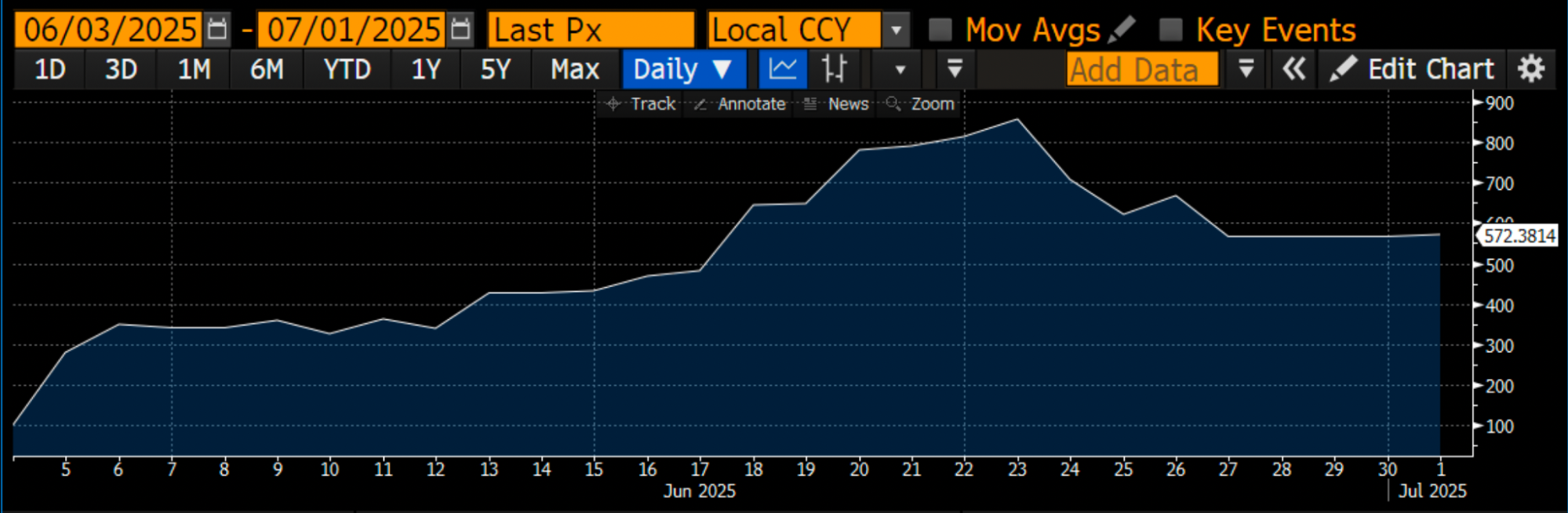

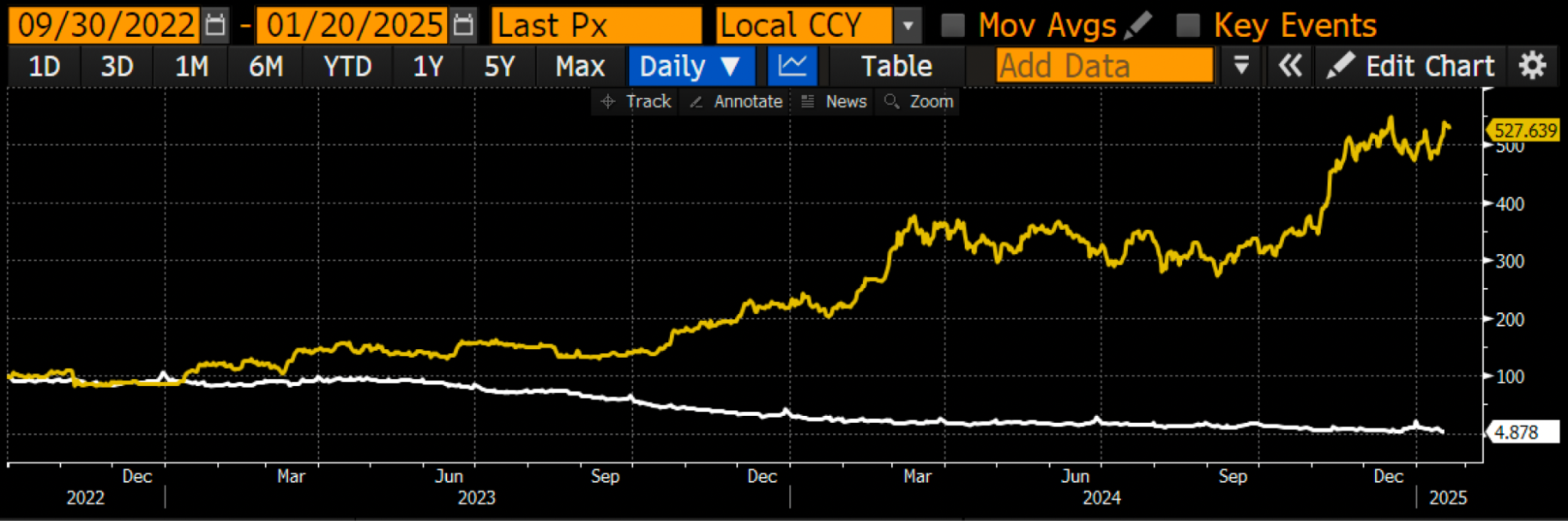

And the result is this chart:

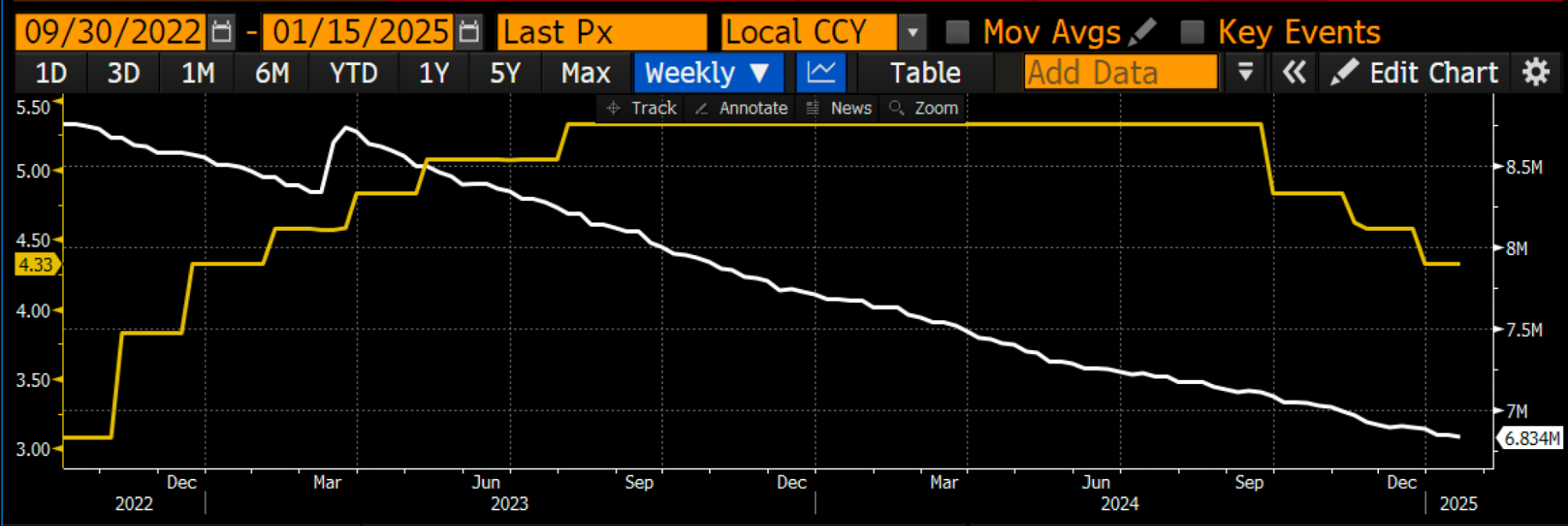

Another result is this sad chart (because I own Bitcoin not $CRCL):

The question crypto degens should ask themselves is why is The BBC so bullish on stablecoins. Why did the Genius Act receive bipartisan support? Is it that American politicians actually care about financial freedom, or is there something else afoot? Maybe politicians do care about financial freedom in the abstract, but lofty ideals do not power action. There must be another, more realpolitik reason for the about-face on stablecoins. Remember in 2019, Facebook’s efforts to integrate a stablecoin called Libra into its social media empire were shuttered due to opposition from politicians and the US Federal Reserve (Fed). Let’s review the major problem the BBC must solve to understand why the BBC is going goo goo gagga gagga over stablecoins.

The major issue that US Treasury Secretary Scott “The BBC” Bessent faces is the same one that his predecessor Janet “Bad Gurl” Yellen faced. Their bosses like to spend money without raising taxes; i.e., the US president and politicians in the House of Representatives and the Senate. It then falls to the Treasury Secretary to fund the government via borrowing at an affordable rate. Very quickly, it became clear that the market does not want to buy long-term government bonds of any over-indebted advanced economy at high prices/low yields. This is the doom porn twerk-off The BBC and Bad Gurl Yellen watched over the past few years … booty booty butt:

If rising yields weren’t bad enough, the real value of these bonds got torched.

Real Value = Bond Price / Gold Price

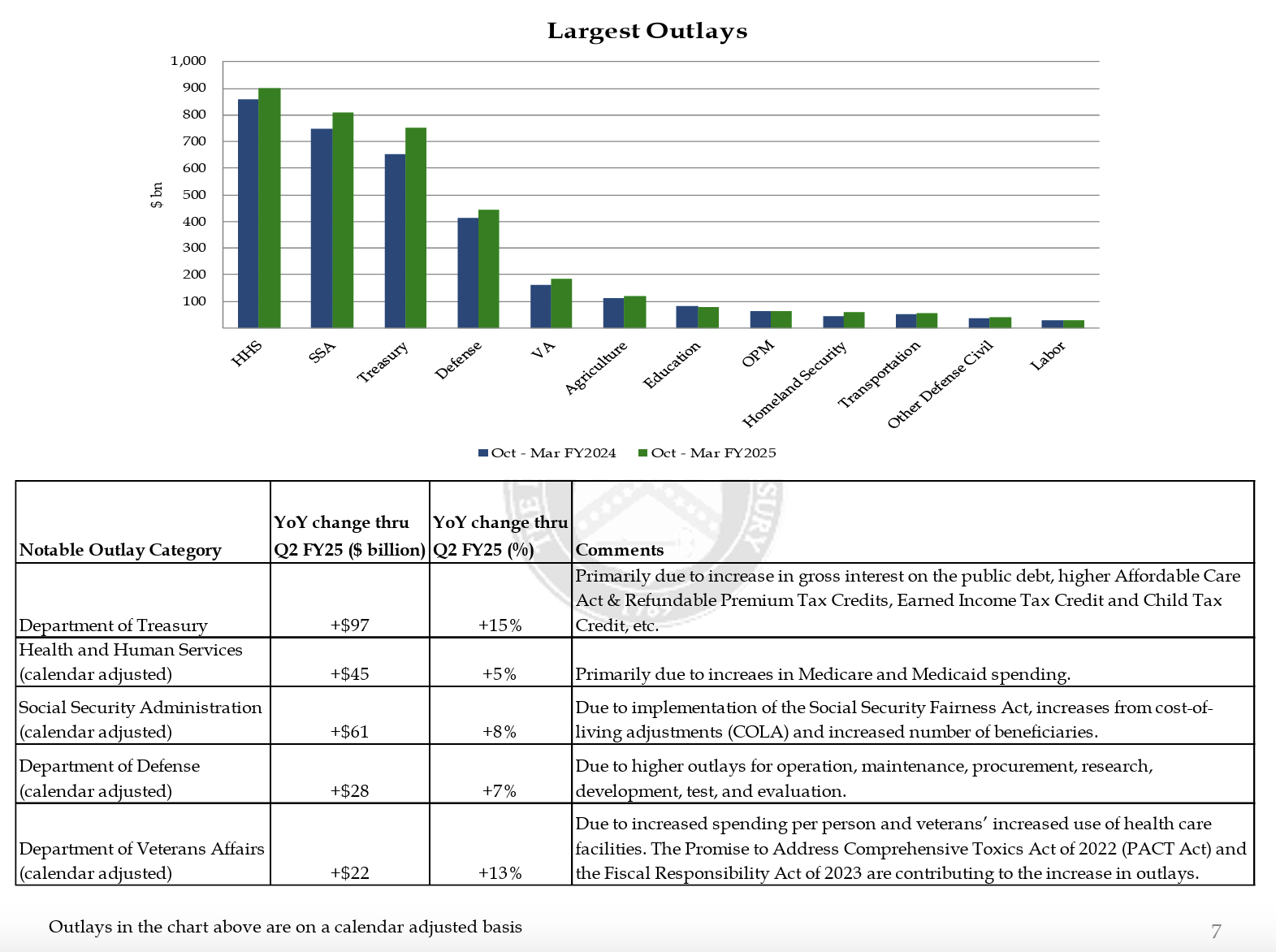

If past performance weren’t bad enough, here are some other constraints faced by Yellen and now Bessent. The bond sales team at the Treasury Department must engineer an issuance schedule that accomplishes the following:

Fund ~$2 trillion of yearly federal deficits plus $3.1 trillion of maturing debt in 2025.

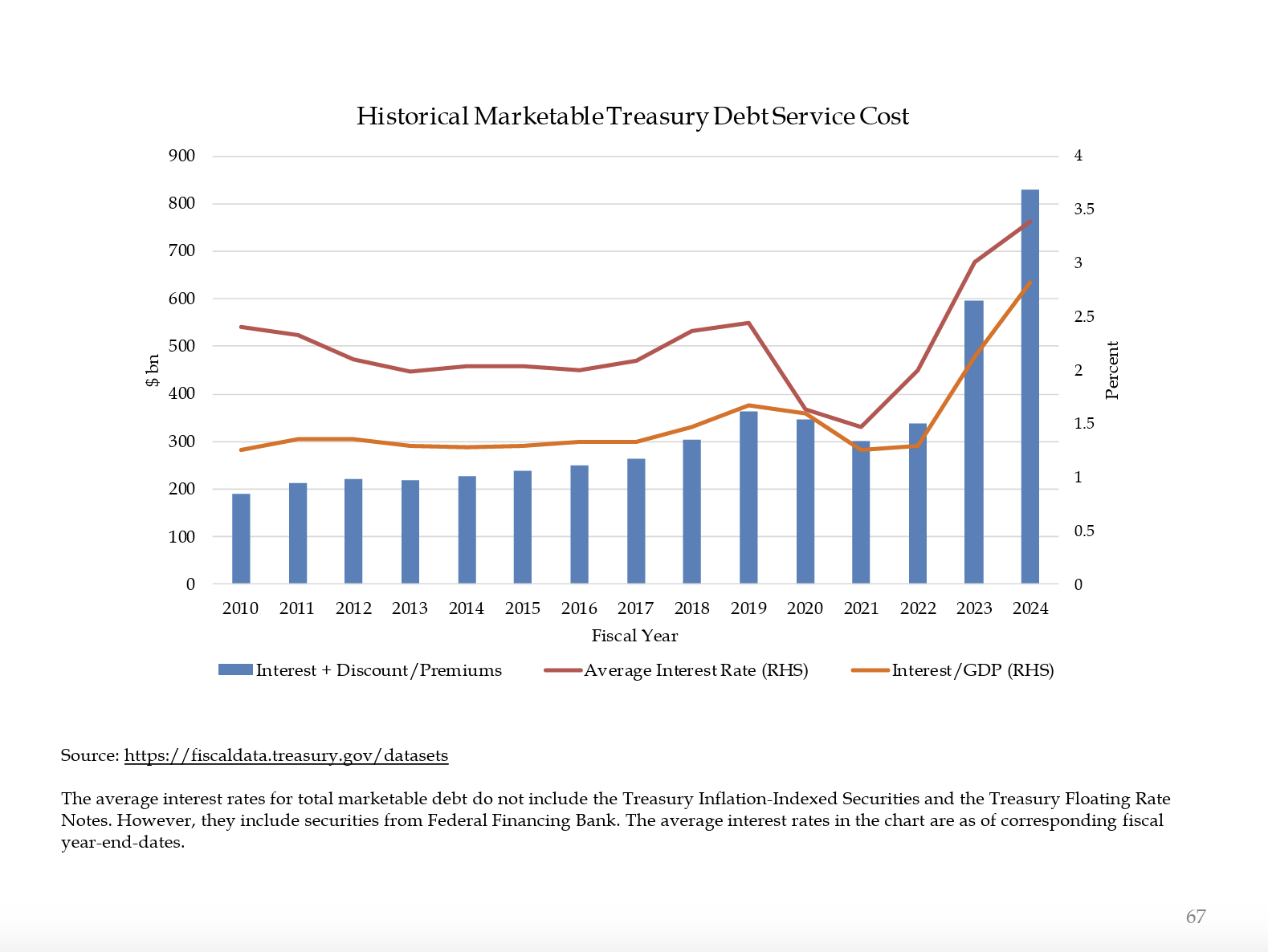

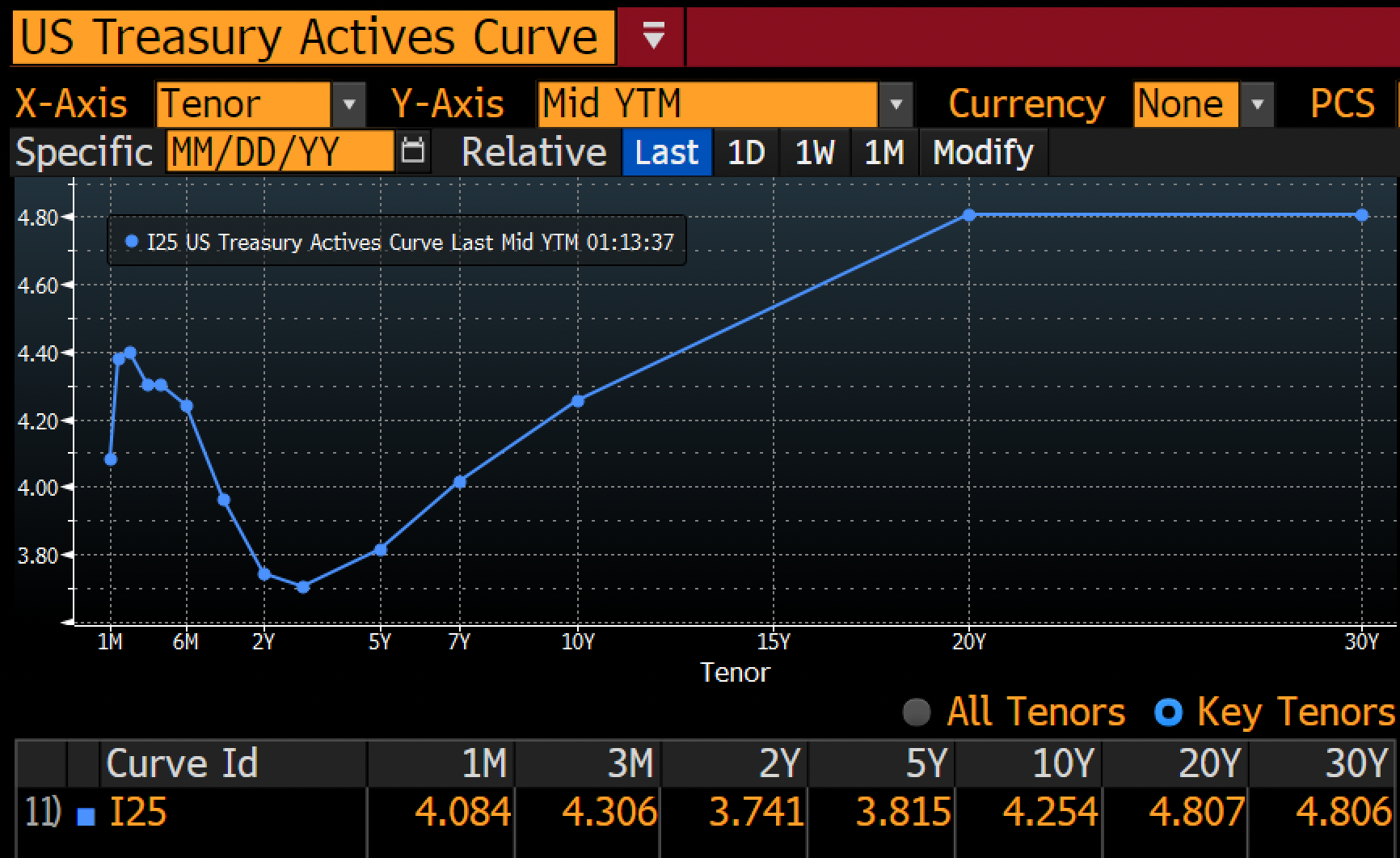

The previous two charts show that the weighted average interest rate paid on outstanding treasury debt is lower than all points on the treasury yield curve.

The previous two charts show that the weighted average interest rate paid on outstanding treasury debt is lower than all points on the treasury yield curve.

- The financial system issues credit collateralized by nominally risk-free treasury debt. Therefore, interest must be paid; otherwise, the government defaults on a nominal basis, which would destroy the entire filthy fiat financial system. The interest expense will continue to increase as maturing debt will be financed at higher rates because the entire treasury yield curve is higher than the current weighted average interest on the debt.

- The defense budget will not go down, given that the US is engaged in wars in Ukraine and the Middle East.

- The healthcare outlays will increase into the early 2030s as baby boomers enter their prime years of receiving sick care from Big Pharma, paid for by the US government.

Sell bonds in such a way that the benchmark 10-year yield does not rise over 5%.

- When the 10-year yield approaches 5%, bond market volatility measured by the MOVE Index spikes, and a financial crisis is not far behind.

Sell bonds in such a way that is stimulative to the broader financial markets.

- The US government requires tax revenue derived from taxing year-on-year stock market gains to prevent truly mind-bogglingly large fiscal deficits.

- The US government exists to serve wealthy property owners. In the good old days when the bitch was in the kitchen, the nigger in the field, and the injun in the hinterland, only white male property owners were allowed to vote. In modern America, while suffrage is universal, power still emanates from the wealth that controls listed corporations, resulting in government policy that enriches and entrenches the power of the roughly 10% of households who control over 90% of stock market wealth. One of the most salient examples of the government’s preference for property owners is how, during the 2008 Global Financial Crisis (GFC), the Fed printed money to save banks and the broader financial system, but the banks were still allowed to foreclose on people’s homes and businesses. Socialism for the rich, capitalism for the poor! With a track record like this, it’s no wonder New York City mayoral candidate Mamdani is so popular; the poor folks want some of that socialism too.

The Treasury Secretary’s job was easy when the Fed was conducting quantitative easing (QE). The Fed printed money and bought bonds, which enabled the US government to gorge itself on cheap debt and levitated the stock market. But now that the Fed, at least optically, must appear to be fighting inflation, the august body cannot cut rates or engage in QE. The Treasury Department must do the heavy lifting all alone.

By September 2022, the market decided to sell bonds on the margin due to the belief in the permanence of the largest peacetime US federal deficits in the country’s history and a hawkish Fed. The 10-year yield almost doubled in two months, the stock market was down close to 20% from the summer highs, then Bad Gurl Yellen put her red bottoms on and got to work. In what has been called Activist Treasury Issuance (ATI) in a paper written by Hudson Bay Capital, Yellen began issuing more treasury bills than those with a coupon. Over the next two years, $2.5 trillion was injected into the financial markets due to the Fed’s Reverse Repo Program (RRP) balance falling. If the goal was ticking the three boxes I outlined above, Yellen’s ATI policy crushed it. That was then, but what about The BBC? How will he tick the same boxes in the current environment? The RRP is practically empty; where will he find trillions of dollars of sterilized funds sitting on a balance sheet ready and willing to buy treasury debt at high prices and low yields?

There are two pools of funds owned by the large Too Big to Fail (TBTF) banks ready and willing, if there is the requisite profit potential, to buy trillions of dollars’ worth of treasury debt. They are demand/time deposits and reserves held at the Fed. I’m focusing on the eight TBTF banks because their existence and profitability are predicated on the government guarantee of their liabilities and banking regulations are crafted to benefit them more so than non-TBTF banks. Therefore, they will do what the government asks as long as there is some modicum of profit on offer. The BBC requests they purchase his shitty bonds, and in return, he will shower them with risk-free returns.

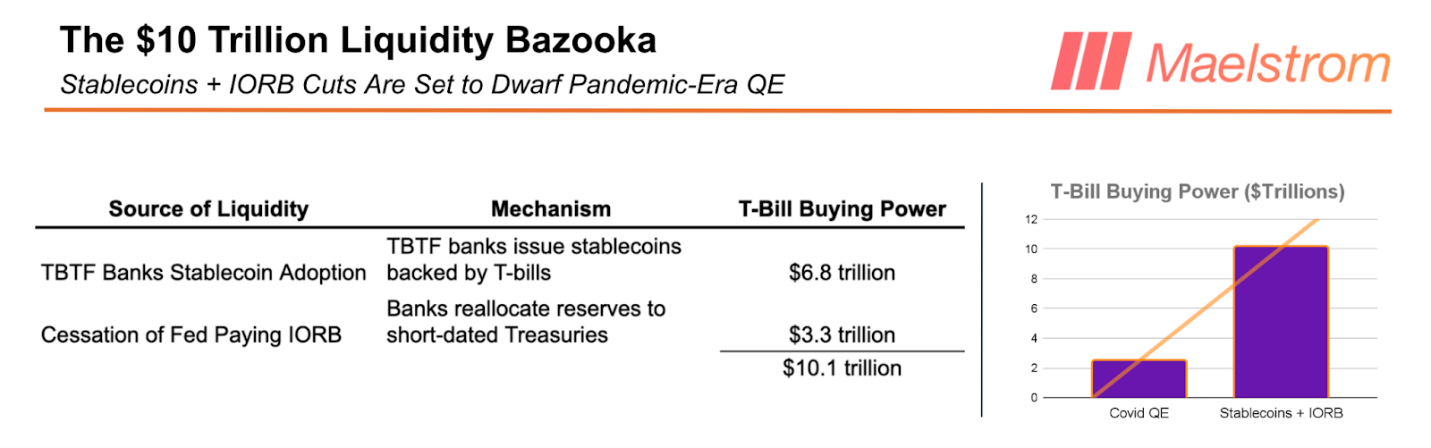

I believe the reason why the BBC is so pumped up about all things “stablecoin” is that by issuing a stablecoin, TBTF banks will unlock up to $6.8 trillion of T-bill purchasing power. These inert deposits can then be re-leveraged within the fugazi fiat financial system to levitate markets. In the next section, I will walk through my model of how the issuance of a stablecoin leads to T-bill purchases and enhanced TBTF banking profitability.

After discussing the stablecoin-to-T-bill flow, I will quickly explain how, if the Fed stops paying interest on reserves, it will free up to $3.3 trillion to buy treasury debt. This will be another example of a policy that technically is not QE, but will have the same positive effect on fixed supply monetary assets like Bitcoin.

Let’s learn about The BBC’s new favourite monetary bazooka, stablecoins.

The Stablecoin Flow

My prediction rests on a few critical assumptions:

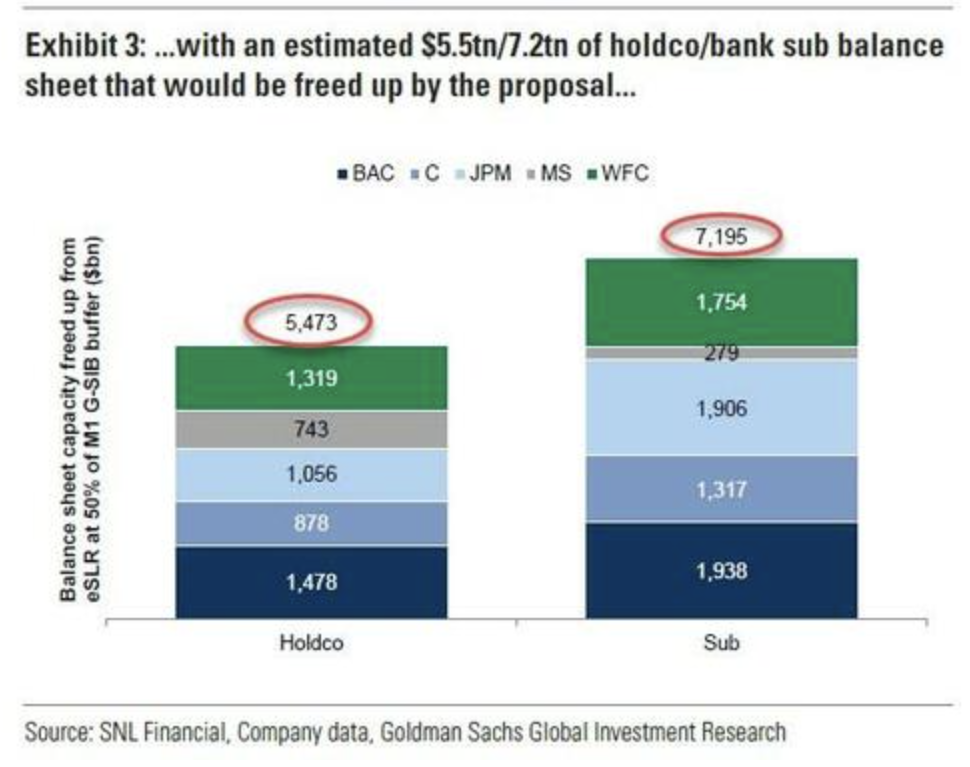

Treasuries Receive a Full or Partial Exemption from the Supplemental Leverage Ratio (SLR)

- An exemption means that a bank is not required to hold equity capital against its treasury portfolio. A full exemption means that banks can buy treasuries with infinite leverage.

- The Fed just voted to reduce the amount of capital banks must hold against treasuries; the first effects will be felt within the next three to six months. It is estimated this proposal frees up $5.5 trillion of bank balance sheet capacity to buy treasuries, as per the chart above. Markets are forward looking so this buying power will begin to be front ran in the treasury market leading to lower yield ceteris paribus.

Banks are Profit-Motivated Loss-Minimizing Organizations

- From 2020 to 2022, banks were urged by the Fed and Treasury to load up on treasuries; banks bought a fuck ton of longer-dated coupon bonds due to their higher yields. By April 2023, losses on these bonds, due to the fastest rise in Fed policy rates since the early 1980s, caused three banks to fail within a week. In the TBTF realm, Bank of America’s losses on its Held to Maturity portfolio of bonds eclipsed its total equity capital and the bank would have been insolvent if forced to mark-to-market its bond portfolio. To squash the crisis, the Fed and Treasury effectively nationalized the entire US banking system via the Bank Term Funding Program (BTFP). Non-TBTF banks can still lose money, however, and if losses on treasuries cause insolvency, management will be ousted and the bank sold to Jamie Dimon or another TBTF bank for a song. Therefore, bank CIOs are hesitant to load up on long-term treasury bonds lest the Fed conducts another rug pull by raising rates.

- Banks will buy T-bills because they are effectively high-yielding zero-duration cash-like instruments.

- Banks will only buy T-bills with deposits if they earn a high net interest margin (NIM) and are required to post little to no capital against them.

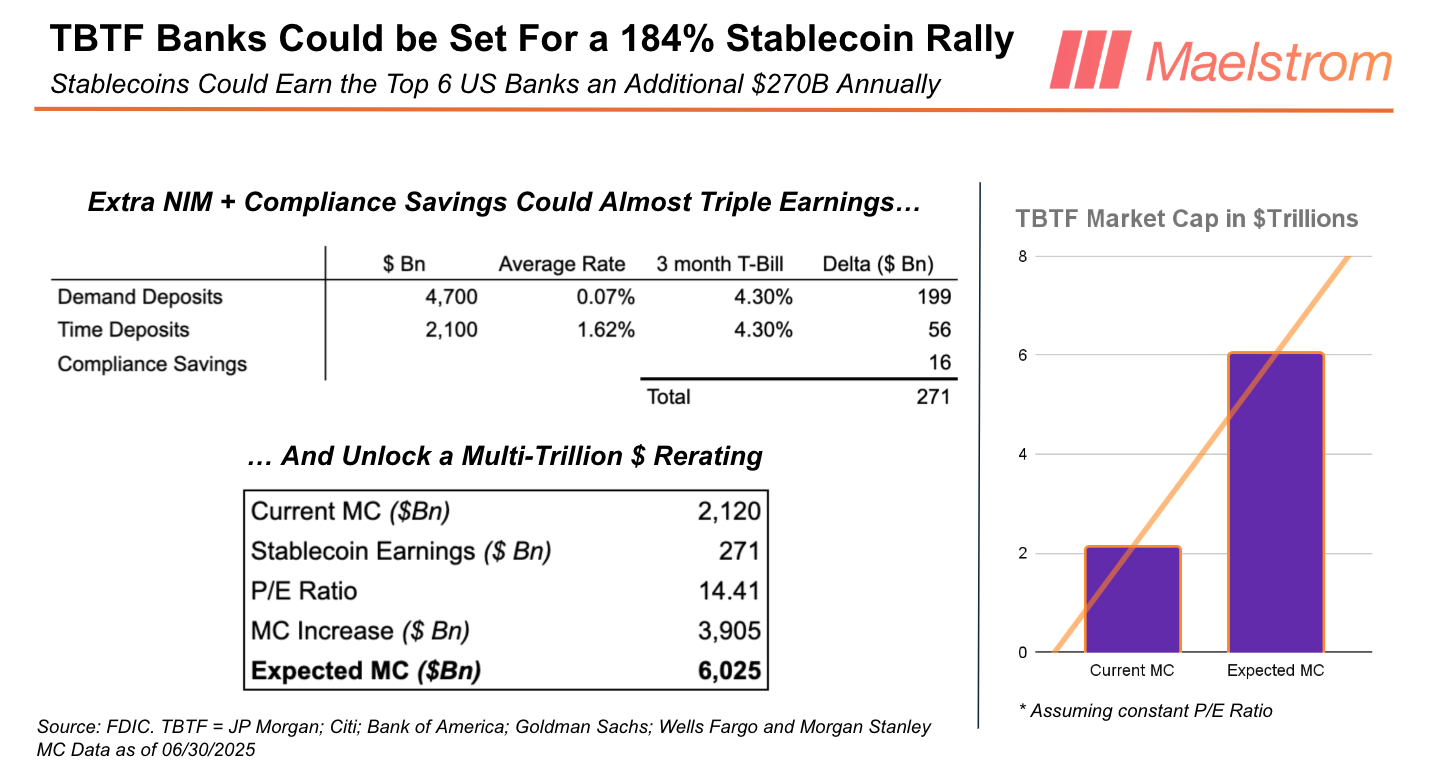

JP Morgan recently announced its plan to launch a stablecoin called JPMD. JPMD will ride on Base, a layer-2 operated by Coinbase built on top of Ethereum. As a result, JP Morgan will have two types of deposits. The first I will refer to as regular deposits. Regular deposits are still digital, but to move them within the financial system requires bank-to-bank antiquated systems talking to each other and a massive amount of human oversight. Regular deposits move Monday to Friday, 9 a.m. to 4:30 p.m. Regular deposits pay a paltry yield; the Federal Deposit Insurance Corporation (FDIC) estimates that the average yield on a regular demand deposit is 0.07% and 1.62% for a one-year time deposit.

The second type of deposit is a stablecoin, or JPMD. JPMD rides on a public blockchain, which in this case is Base. Customers can spend their JPMD 24/7, 365. JPMD, by law, cannot pay a yield, but I imagine that JP Morgan will entice customers to convert regular deposits into JPMD by offering generous cash-back spending perks. It is unclear at the current moment whether offering a staking yield is allowed.

Staking Yield: This is when a customer locks up their JPMD with JP Morgan; while the stablecoin is locked, it receives yield.

Customers move money from regular deposits to JPMD because JPMD is more useful and the bank offers cash-back spending perks. In total, the TBTF banks have an estimated $6.8 trillion in demand and time deposits. Very quickly, because stablecoins are a better product, regular deposits will be converted to JPMD or similar stablecoins issued by other TBTF banks.

Why would JP Morgan go through the hassle of nudging customers to switch from regular deposits to JPMD? The first reason is cost reduction. If all regular deposits become JPMD, then JP Morgan can effectively eliminate its compliance and operations departments. Let me explain why Jamie Dimon came in his pants when he learned about how stablecoins actually work.

Compliance at a high level consists of a set of rules handed down by regulators and enforced by a horde of humans using technology from the early 1990s. The structure of rules takes the form of: if this happens, then do that. These if/then relationships can be interpreted by a single senior compliance officer and codified into rules that an AI agent can follow flawlessly. Because JPMD offers full transparency due to the fact that all public addresses are doxxed, an AI agent trained on the corpus of relevant compliance regulations can perfectly ensure that certain transactions are never approved. The AI can also instantaneously prepare any report requested by a regulator. The regulator, in turn, can validate the correctness of the data because it all exists on a public blockchain. In aggregate, the TBTF banks spend $20 billion per year on compliance and the operations and technology required to comply with banking regulations. This will be reduced to effectively zero by shifting all regular deposits into stablecoins.

The second reason why JP Morgan will push JPMD is that it allows the bank to purchase billions of dollars’ worth of T-bills risk-free with the stablecoin assets under custody (AUC). This is because T-bills have close to zero interest rate risk but effectively yield the Fed Funds Rate. Remember that TBTF banks have $5.5 trillion of treasury buying capacity under the new SLR. The banks need to find a pot of inert cash with which to purchase said debt, and deposits held by their stablecoin are a perfect fit.

Some readers might retort that JP Morgan can already buy T-bills with its regular deposits. My response is that stablecoins are the future because they create a better customer experience and allow TBTF banks to eliminate $20 billion of costs. This cost savings alone will motivate banks to embrace stablecoins; the extra NIM is the cherry on top.

I know that many readers want to splunk their hard-earned cash into Circle ($CRCL) or the next shiny new stablecoin issuer. But don’t sleep on the stablecoin profit potential for TBTF banks. If we take the average price-to-earnings ratio of the TBTF banks at 14.41x and multiply that by the cost savings and stablecoin NIM potential, it comes out to $3.91 trillion. The current market cap of the eight TBTF banks is approximately $2.1 trillion, which means that stablecoins could pump TBTF bank stocks on average by 184%. If there is a non-consensus trade out there an investor can execute in SIZE, it is going long an equally weighted basket of the TBTF banks based on this stablecoin thesis.

What about competition?

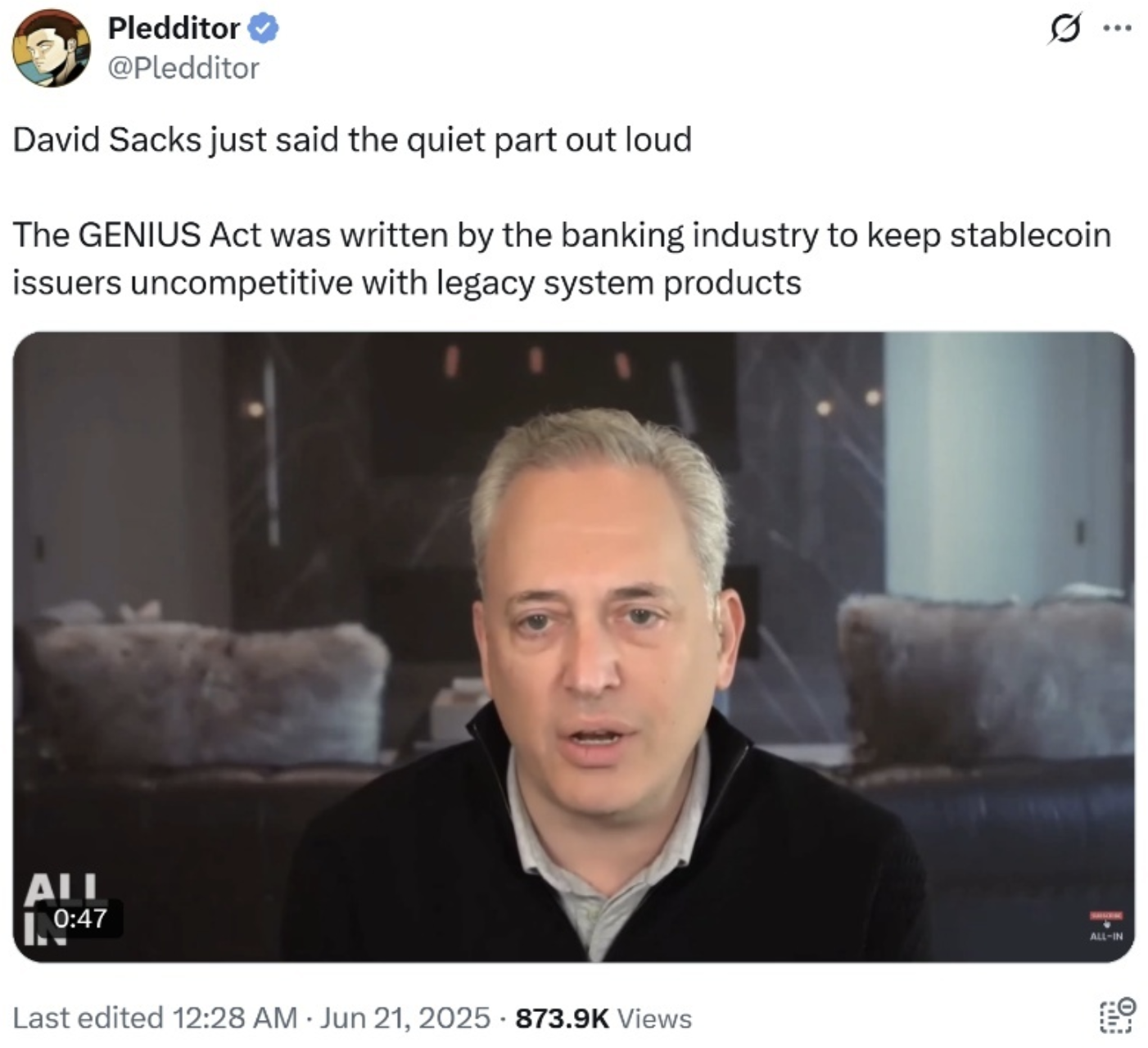

Don’t worry about that; the Genius Act ensures that non-bank-issued stablecoins cannot compete at scale. The act explicitly bars technology firms like Meta from launching their own stablecoins; they must partner with a bank or FinTech. Of course, anyone can in theory obtain a banking charter or purchase an existing bank, but all new owners must be approved by the regulators. Let’s see how long that takes. Another provision that hands the stablecoin market to banks is the prohibition on paying interest to stablecoin holders. Without the ability to compete on interest payments to holders, FinTechs will not be able to affordably siphon deposits away from banks. Even successful issuers like Circle will never be able to tap into the $6.8 trillion worth of TBTF regular deposits up for grabs. Furthermore, FinTechs like Circle and smaller banks do not enjoy a government guarantee of their liabilities, but TBTF banks do. If my mother were ever going to use a stablecoin, it would be one issued by a TBTF bank. Boomers like her will never use a FinTech or smaller bank for this purpose because they don’t trust them due to the lack of a government guarantee.

David Sachs, the US President Trump’s Crypto Czar, agrees. I’m sure many corporate crypto donors are miffed that after all those crypto campaign donations the result was being quietly shut out of the lucrative US stablecoin market. Maybe they should change tactics and actually advocate for true financial freedom, and not for just a stool under the chamber pot where the TBTF bank CEOs defecate.

In short, the adoption of stablecoins by TBTF banks eliminates FinTech competition for their deposit base, reduces the need for expensive human and routinely incompetent compliance officers, requires no payment of interest which boosts their NIM, and ultimately results in their stock price pumping. In return for the gift of stablecoins bequeathed by The BBC, TBTF banks will purchase up to $6.8 trillion worth of T-bills.

In short, the adoption of stablecoins by TBTF banks eliminates FinTech competition for their deposit base, reduces the need for expensive human and routinely incompetent compliance officers, requires no payment of interest which boosts their NIM, and ultimately results in their stock price pumping. In return for the gift of stablecoins bequeathed by The BBC, TBTF banks will purchase up to $6.8 trillion worth of T-bills.

ATI : Bad Gurl Yellen : Stablecoins : The BBC

Next up, I will talk about how the BBC can liberate another $3.3 trillion of inert reserves from the Fed’s balance sheet.

Interest on Reserve Balances (IORB)

In the aftermath of the 2008 GFC, the Fed decided that banks would never go under for lack of reserves. The Fed creates reserves that sit dormant on its balance sheet by purchasing treasuries and mortgage-backed securities from banks; this is called quantitative easing. The banks can, in theory, convert reserves held at the Fed into currency in circulation, which can be lent out, but decline to do so because the Fed prints money to pay them sufficient interest. The Fed sterilizes these reserves to prevent inflation from spiking even higher. The problem for the Fed is that the interest on reserve balances (IORB) increases as they raise rates. This is not good because unrealized losses on the Fed’s bond portfolio also increase as it raises rates. As a result, the Fed is insolvent and operating in a negative cash flow situation. The negative cash flow situation is purely a policy choice that can be changed, however.

US Senator Ted Cruz recently mused that maybe the Fed should cease paying IORB. That would force banks to replace that lost interest income by converting reserves into treasuries. Specifically, I argue they will purchase T-bills due to their high-yielding, cash-like properties.

Sen. Ted Cruz has been pushing his Senate colleagues to end the power to pay banks reserves out of a belief that this change would be a big contributor to lowering deficits.

– Source: Reuters

Why should the Fed print money and prevent the banks from supporting the empire? There is no reason for a politician to oppose this policy change. Both Democrats and Republicans love fiscal deficits; why not allow themselves to spend more by unleashing $3.3 trillion worth of bank buying power into the treasury market? Given that the Fed is unwilling to help Team Trump finance America First, I believe that Republican legislators using their majorities in both legislative houses will strip the Fed of this power. Therefore, the next time yields spike, lawmakers will stand ready to unleash this torrent of money to finance their wanton spending.

Before I conclude this essay by waxing bullish on the dollar liquidity that will surely get created during The BBC’s tenure, I want to talk about Maelstrom’s cautious positioning between now and the third quarter.

A Cautionary Tale

While I am very bullish, I believe there could be a short lull in dollar liquidity creation after Trump’s spending bill, called the Big Beautiful Bill, is passed.

The bill, as it currently reads, raises the debt limit. While many provisions will be horse-traded among the politicians, Trump will not sign a bill that doesn’t hike the debt ceiling. He needs additional borrowing capacity to fund his agenda. There is no indication that the Republicans will attempt to force the government to contract spending. The question for traders is, what is the dollar liquidity impact when the Treasury resumes net borrowing?

The Treasury continued to fund the government from January 1st onwards primarily by drawing down its checking account, the Treasury General Account (TGA). The TGA balance is $364 billion as of June 25th. As per guidance from the Treasury Department in its most recent quarterly refunding announcement, if the debt ceiling were raised today, the TGA balance would be refilled to $850 billion by issuing debt. This would cause a dollar liquidity contraction of $486 billion. The only major dollar liquidity line item that could soften the negative impulse is if funds leave the RRP, which stands at $461 billion.

This is not a slam dunk Bitcoin short trading setup due to the TGA refill. This is a proceed with caution; the bull market might be interrupted for a short period of time trading setup. I believe that between now and the August Jackson Hole Fed speech to be given by beta cuck towel bitch boy Jerome Powell, the market will trade sideways to slightly lower. If the TGA refill proves to be dollar liquidity negative, then the downside is $90,000 to $95,000. If the refill proves to be a nothingburger, Bitcoin will chop in the $100,000s without a decisive break above the $112,000 all-time-high. I have a feeling that Powell will announce the end of quantitative tightening and/or other what will seem to be mundane but highly significant banking regulatory changes. By early September, the debt ceiling will have been raised, the TGA mostly refilled, and the Republicans laser-focused on handing out goodies so they don’t get Mamdani’d in their home district come November 2026. Then green dojis will impale the bears powered by a surge in money creation.

Between now and the end of August, Maelstrom will be overweight staked USDe (Ethena USD). We already dumped all our liquid shitcoin positions. Depending on the price action, we may lighten up on Bitcoin risk as well. Buying shitcoin risk on or around April 9th yielded 2x-4x gains on a select number of shitcoins within three months. Without a clear liquidity catalyst, the shitcoin complex will get smoked. In the aftermath, we can dumpster dive with confidence and maybe hit a five or ten bagger before there is another lull in fiat liquidity creation in the late fourth quarter of 2025 or early first quarter of 2026.

Tick the Boxes

Adoption of stablecoins by TBTF banks creates up to $6.8 trillion of T-bill buying power.

Cessation of the Fed paying IORB creates up to $3.3 trillion of T-bill buying power.

$10.1 trillion can flood into the T-bill market over time due to the BBC’s policies. If my predictions are correct, this $10.1 trillion liquidity injection will act upon risky assets in the same way Bad Gurl Yellen’s $2.5 trillion injection did… PUMP UP THE JAM!

This is yet another liquidity arrow that can be plucked from The BBC’s policy quiver when needed. It will be needed once Trump’s Big Beautiful Bill is passed and the debt limit raised. Quickly thereafter investors will start to fret again on how in the fuck the treasury market is supposed to digest the massive amount of to be issued debt without imploding.

Some of you are still waiting for monetary Godot. You are waiting for Fed Chairperson Powell to announce another round of unlimited QE and rate cuts before you sell bonds and buy crypto. It ain’t happening, at least not until the US definitely enters a kinetic war against Russia, China, and/or Iran, or a large systemically important financial institution is on the brink of collapse. Not even a recession will bring Godot into being. So, stop listening to the simp sitting in the cuck chair, and start listening to the man wielding the monster cock.

Some of you are still waiting for monetary Godot. You are waiting for Fed Chairperson Powell to announce another round of unlimited QE and rate cuts before you sell bonds and buy crypto. It ain’t happening, at least not until the US definitely enters a kinetic war against Russia, China, and/or Iran, or a large systemically important financial institution is on the brink of collapse. Not even a recession will bring Godot into being. So, stop listening to the simp sitting in the cuck chair, and start listening to the man wielding the monster cock.

The next few charts will show the opportunity cost investors suffered waiting for monetary Godot.

Do not make the same mistake again. Many financial advisors are still pushing clients to buy bonds because yields are forecast to fall. I agree that central banks globally will cut rates and print money to prevent the meltdown of their government bond markets. Furthermore, if the central bank doesn’t do something, finance ministries will. That is the argument I put forward in this essay; I believe Bessent, via support for stablecoin regulation, SLR exemptions, and cessation of paying IORB, can unleash up to $10.1 trillion of buying power for treasuries. But who cares if you make 5% or 10% returns being long bonds? You will miss out on Bitcoin pumping 10x to $1 million or the Nasdaq 100 spiking 5x to 100,000 by 2028.

The real stablecoin play isn’t betting on crusty FinTechs like Circle—it’s understanding that the US government just handed TBTF banks the launch keys to a multi-trillion-dollar liquidity bazooka disguised as “innovation.” This isn’t DeFi. This isn’t financial freedom. This is debt monetization dressed in Ethereum drag. And if you’re still waiting for Powell to whisper “QE infinity” in your ear before you go risk-on, congrats—you’re the exit liquidity.

Instead go long Bitcoin. Go long JPMorgan. Forget about Circle. The stablecoin Trojan horse is already inside the fortress, and when it opens, it’s not armed with libertarian dreams—it’s loaded with T-bill buying liquidity aimed at keeping equities inflated, deficits funded, and Boomers sedated. Don’t sit on the sidelines waiting for Powell to bless the bull market. The BBC is done getting fluffed, and it’s time for him to soak the world with his liquidity juices.

Want More? Follow the Author on Instagram, LinkedIn and X

Access the Korean language version here: Naver

Subscribe to see the latest Events: Calendar